.svg)

.svg)

.png)

Payday Super is the most significant change to superannuation obligations for Australian employers in years. From 1 July 2026, Super Guranteee (SG) contributions will need to reach your employees' funds within days of each pay run, not at the end of the quarter.

To help businesses get across the changes, Microkeeper and Beam have put together answers to the questions employers are asking most. Here's everything in one place.

1. How long do employers have to get super to the fund under payday super?

No later than 7 business days after payday, with payday counted as day zero.

This is a fundamental shift. Under the current quarterly model, super is a separate task that gets processed well after employees are paid. Under payday super, the clock starts the moment you pay your employees, and contributions need to be initiated, processed through a clearing house, and received by the fund, all within that window.

For most businesses, this means super needs to be built directly into the standard payroll workflow. If your payroll software and clearing house are properly integrated, the process can be largely automated. The key is making sure your employee data is clean and contribution files are error-free before payday super starts, because there’s no longer enough time to identify and fix errors once a pay run is processed.

2. What new concept replaces Ordinary Time Earnings?

Qualifying earnings (QE) replaces Ordinary Time Earnings (OTE) as the basis for calculating the super guarantee under payday super.

While similar in concept, qualifying earnings is broader. It includes standard OTE but also captures commissions earned outside of ordinary hours and certain salary sacrificed amounts that were previously excluded from OTE calculations.

For payroll teams, this is worth paying close attention to. Employees paid commissions or those with salary sacrifice arrangements may see changes to their SG calculations. Confirm with your payroll provider that their software is being updated to reflect qualifying earnings ahead of the July start date.

3. How quickly do super funds need to allocate contributions?

Under payday super, funds have just 3 business days to allocate a contribution to a member’s account, or return it to the employer if it can’t be allocated. That’s down from the current 20 business days.

For employers, the implication is twofold. First, you’ll find out about rejected contributions much faster. Second, you’ll have less time to act on them, a returned contribution still needs to reach the fund within the original 7-business-day window.

This is one of the key reasons having a clearing house that handles returns and resubmissions automatically becomes genuinely important under payday super, not just convenient.

4. The ATO Small Business Superannuation Clearing House is closing, what now?

The ATO Small Business Super Clearing House (SBSCH) closes on 30 June 2026, ahead of payday super commencing in July.

If your business has been using the SBSCH, available to businesses with fewer than 20 employees or annual turnover under $10 million, you’ll need to move to an alternative clearing house before the date.

The SBSCH was designed around the quarterly super model. Payday super requires faster processing, better error handling, and tighter integration with payroll software. If you haven’t started evaluating alternatives yet, now is the time, migrating employee and fund data takes longer than expected, and June 2026 is a hard deadline.

5. What's the window for a new employee's first contribution?

Employers have 20 business days from a new employee’s first payday to ensure their first SG contribution reaches their super fund. After that initial contribution, the standard 7-business-day rule applies to every subsequent pay run.

The 20-day window exists to give employers time to complete fund nomination, verification, and member checks. But it’s not a reason to wait. The best approach is to treat super setup as part of day-one onboarding, collect fund details, run a Member Verification Request, and have everything confirmed well before the first payday arrives.

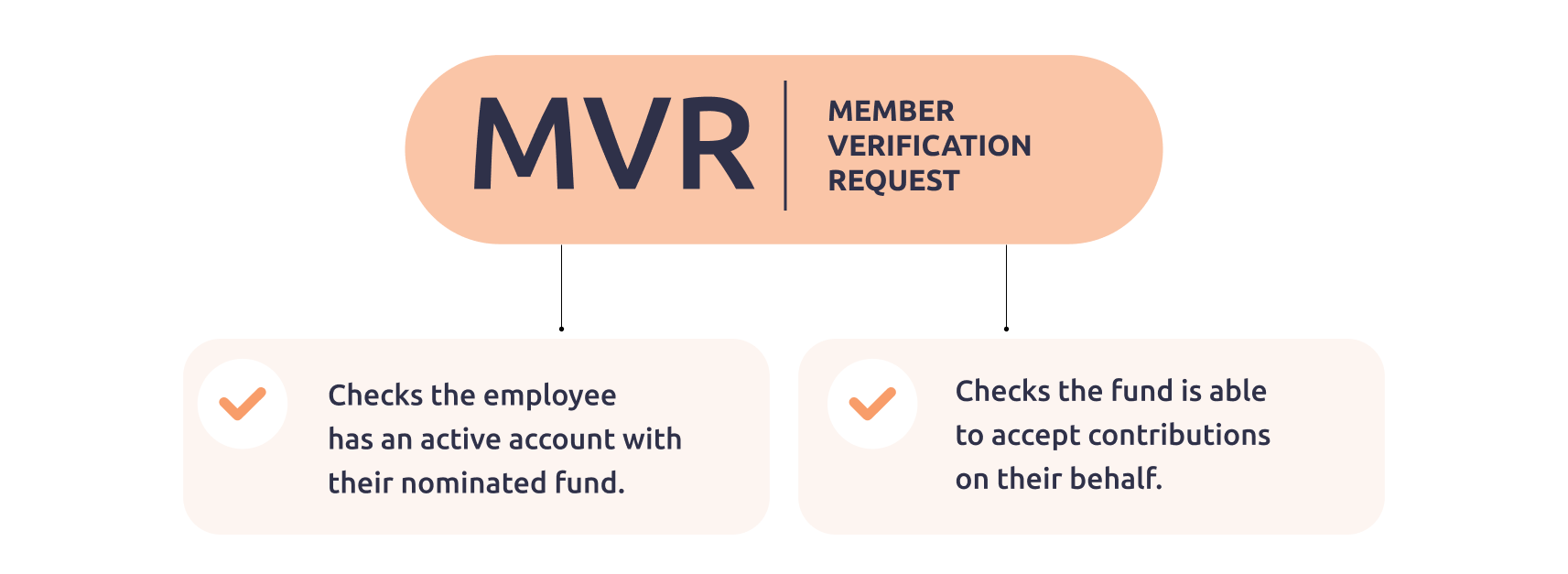

6. What is a Member Verification Request?

A Member Verification Request (MVR) is a new mandatory step that employers must complete before making an SG contribution for a new employee for the first time.

The MVR confirms two things: that the employee has an active account with their nominated fund, and that the fund is able to accept contributions on their behalf. Running this check upfront significantly reduces the risk of contributions being rejected after payment, one of the most common compliance headaches under the current system.

Think of the MVR as a standard part of employee onboarding, sitting alongside collecting a TFN and bank details. The earlier it’s completed, the more time you have to resolve any issues before the employee’s first payday.

7. How is the Maximum Contribution Base changing?

The Maximum Contribution Base (MCB), the earnings threshold above which the super guarantee is not required, is moving from a quarterly to an annual calculation. It is expected to be set at $250,000 for FY27.

For most businesses, the practical impact is minimal. But for employees with higher salaries, variable earnings, or income that fluctuates significantly across the year, the shift to an annual MCB can affect how much super you’re obligated to contribute at different points in the year.

If you have employees whose earnings are close to or above the MCB, it’s worth confirming how your payroll software will handle the annual calculation. This should be managed automatically by your provider, but it’s worth verifying.

8. What's the best way to prepare for payday super right now?

.png)

The most valuable thing any business can do before payday super starts is audit employee data and check contribution files for existing errors.

Under the quarterly model, there’s time between payments to identify and fix data issues. Under payday super, that buffer disappears. An incorrect fund detail, an outdated member number, or a missing TFN becomes a problem that needs to be resolved within 7 business days.

A practical pre-July checklist:

- Check all employee super fund details are current and correct.

- Follow up any employees who haven’t completed a Choice of Fund form.

- Review previous contribution files for warnings or errors and resolve them now.

- Confirm your clearing house is set up and integrated with your payroll software.

- Run Member Verification Requests for new employees as part of standard onboarding.

Clean, accurate data going into July means far fewer issues once the 7-day clock is running on every pay run.

Microkeeper and Beam are ready for Payday Super

Microkeeper’s integration with Beam is built and ready for a payday super environment. Super contributions are initiated directly from your Microkeeper payrun and processed through Beam’s clearing house automatically, no manual steps, no separate logins, no chasing payment confirmations.

That means the 7-day business window, Member Verification Request, contribution error handling, and resubmissions are all managed within the one workflow your payroll team already uses. When payday super starts in July, businesses on Microkeeper and Beam won’t need to change how they work, the platform handles the compliance requirements in the background.

If you’re not yet set up with Microkeeper and Beam, now is the right time to get everything in place before July. Start a free trial at info.microkeeper.com.au, or get in touch with our team to walk through your current setup and make sure you’re ready.

The blog is provided by Microkeeper. The information about Beam in the blog is provided by Precision Administration Services Pty Ltd (ABN 47 098 977 667, AFSL 246 604) (Precision), issuer of Beam. Microkeeper does not provide advice or a recommendation in relation to Beam or any other clearing house product. The opinions and comments shared by people in this article are theirs alone, and they’re not necessarily shared by Precision.

Precision is wholly owned by Australian Retirement Trust Pty Ltd (ABN 88 010 720 840, AFSL 228 975), trustee of Australian Retirement Trust (ABN 60 905 115 063). The information about Beam is general information only. It’s not based on the specific objectives, financial situation or needs of your business. So think about those things and read the Product Disclosure Statement (PDS) before you make any decision about Beam products. For a copy of the Beam Clearing House PDS, contact Microkeeper or visit their website.

.png)

.png)